Unit-5 Revenue control, Control System-Operating ratios

Unit-5

Revenue control, Control System-Operating ratios

Introduction-

To control the revenue of a unit attention must be paid to the major factors which can have an influence on the profitability. Therefore it is essential to control the main factors which can affect the revenue of a business such as menu beverage list, the total volume of food and beverage sales, the sales mix, the average spend of customers in each selling outlet at different times of the day, the number of covers served and gross profit margins.it is important to note, particularly in commercial operations that somewhere in the total control system there is a need for the accountability of what has been served to the customer and the payment for what has been issued from the kitchen or the bar.

The payment for food and beverage may be made in many forms such as cash, foreign currency, credit cards, cheques travelers’ cheques, lunch type vouchers and signed bills.

All staff handling cash should be adequately trained in the respective companies’ method. It is a common practice for a cashier handbook manual to be produced so that an established procedure may be followed with the specific aim of ensuring that cash security is always efficiently carried out . artificial handbook contains information on the standard procedure to be followed for such things as:

1. Opening procedures-instructions here would include procedures about checking the float, having a float of specific denominations, checking the till roll recording waiters bill pad numbers etc.

2.Working Procedures- instructions on how to accept payment and the procedure to follow.

3.Procedure for accepting foreign currency-what currency is to be accepted, how to obtain the current exchange rate, how this is to be recorded.

4. Closing Procedures- instruction on any documentation and recordings to be completed,catching up recording of credit cards, cheques.

5. Procedure for accepting Credit card- which credit cards are to be accepted, how they are to be checked, method of processing credit cards for payment recording of credit card vouchers.

6. Procedure for accepting vouchers such as lunch vouchers- which voucher are accepted, how this to be recorded.

7. Procedure for accepting Cheques- how check is to be made out, customers to produce a valid cheque guarantee card, checking that signature correspond.

8. Procedure for accepting traveler’s cheques- what travelers’ cheques are acceptable, what currencies are acceptable, witnessing and checking signature, how this is to be recorded.

9. Procedure for accepting complimentary or signed bill- cheque against current list of authorized persons and their signature, how this is to be recorded.

There are two basic approaches to recording and controlling food and beverage sales-

1. A manual system, which is commonly used in small and in exclusive type catering units.

2. An automated system, which is commonly used in units with several outlets, in unit with a high volume of business and in up to date companies with many units.

Manual Systems-

Sales Checks-

one of the simplest steps to take when attempting to establish says control procedure is to require that each item ordered and its selling price are recorded on a winter's sales check.

Using some forms of a check system service the following functions:

1. To remind the waiting staff of the order they have taken.

2. To give a record of sales so that portion sales and sales mixture and sales histories can be.

3. To assist the cashier and facilitate easy check of price charged.

4. To show the customer a detailed list of charges made.

An additional aid is to use numbered checks and control these tightly recording all cancel and missing checks.

It is more common to find duplicate or triplicate checks being used as an aid to control for the following reasons-

1. They provide the kitchen, buffet or bar without written record of what has been ordered and issued.

2. They authorized the kitchen buffet or bar to issue the food and beverage.

3. They provide the opportunity to compare the top copy of the check with the duplicate to ensure that all that has been issued has been charged and paid for.

The Cashier Role-

In addition to following precisely the unit’s procedures for the handling of all revenue transactions, within the restaurant or bar, it is normal practice for the cashier working a manual system to be required to complete the following:

1. To issue cheque pad to the waiting staff prior to a meal period, to record the numbers of the cheque issued in each pad and obtain the waiting staff signature for them; and on the completion of the mail period to receive from the waiting staff their respective unused check pads record the numbers and sign for the receptor of those returned.

2. To check the pricing extension and subtotal of all checks and to add any government tax charges and to enter the total amount due.

3. To receive and check money, credit or, when applicable, an approve signature in payment for the total amount due for each check.

4. To complete the necessary paying in of all cash etc,.In accordance with the unit system list practice. This could be due to a Bank whether a small independent unit or a unit of large company.

Problems of the manual system

In brief, the basic problems of controlling any Food and Beverage corporation are:

1. The time span between purchasing, receiving, sorting, processing, selling the product and obtaining the cash or credit for the product is sometimes only a few hours.

2. The number of items held in stock and at any time is high.

3. A large number of finished items are produced from a combination of large number of items held in stock.

4. The number of transactions taking place on an early basis in some operation can be very high.

5. To be able to control the operation efficiently, management ideally requires control in formation of many types to be available quickly and to be presented in a meaningful way.

The full manual control of food and beverage operation would be costly, time consuming and that are produced would frequently be far too late for meaningful management action to take place. Certain aspect of control such as regular regularly updating the costing of standard recipes, calculating gross profit potentials and providing detail sales. analysis would seldom be done because of the time and labour involved.

A manual system providing a restricted amount of basic data is still widely used in small and medium sized unit although they are likely to be replaced in the near future by machine or electronic system.

The day today operational problem of manual system is many and include such common problems as:

1. Poor handwriting by writing staff resulting in:

(a) Incorrect order given to the kitchen or dispense bar.

(B). From Food bank offer to the customer.

(C). Polly presented for the customer etc.

2. Human error can produce such mistakes as:

(a). Incorrect prices charged to item on a bill

(b). Incorrect additions to a customer's bill.

(c). Incorrect service charge made.

(d). Incorrect government tax charged made.

3. The communication between departments such as restaurant, dispense bar kitchen and cashier has to be done physically by the waiting staff going to the various departments. This is not only time consuming but inefficient.

4. Manual systems do not provide any quick management information data, any data produced at best being normally 24-48 hours old, as well as being costly to produce.

5. Manual system must be restricted to the bare essentials because of the high cost of labour that would be involved in providing detail up to date information.

Machine Systems-

Pre-Checking system-

Precheck machines are somewhat similar in appearance to a standard cash register and are designated to operate only when a cystic is inserted into the printing table to the side of the machine.

The machine is operated in the following way-

1. A server has his own machine key.

2.A check is inserted into the printing table and the particular keys, depending on the order taken, are pressed given an item and price record as well as recording the table number the number of cover and the it is reference number.

3. A duplicate is printed and issued by the machine which is then issued as a duplicate check to obtain food and beverage.

4. For each transaction reference number is given on the sales check and the duplicate.

5. All data is recorded on a continuous audit tape that can be removed only by authorized persons at the end of the day when the machine is cleared, and the total sale taken and compared to actual cash received.

The advantages of the system are:

1. The sales check is made out and record of it made on the additive before the specific system can be obtained from the kitchen or bar

2. Analysis of total sale as per server is made on the audit tape at the end of the each shift.

3. No cashier is required as each server acts as his on cashier, each keeping the cash collected from customer until the end of the left and then paying it on.

4. As each server has on security key to operate the machine, there is restricted access to the machine and no other way by which prechecks can be provided and used in exchange for items from the kitchen or bar.

Preset Prechecking system-

This is an update on the basic precheck machine. The keyboard is much larger than the previous machines and has descriptive keys corresponding to all items on the menu which are processed to the current price of each time. A server pressing the key for, say cheeseburger would not only have the item printed out but also the price. A control panel, kept under lock and key, would enable management to change the price of any time, if required very quickly. It is also possible to have a running count kept of each item recorded and at the end of a meal period by depressing each ki intern to get a printout giving a basic analysis of sales made.

Electronic cash register (ECRs) –

These are very high-speed machines which work development for operations such as supermarkets and were for the adapted for use in high volume catering operations.

The particular advantages of these machines are that they will:

1. Price customers check through preset or buy price look-ups.

2. Print cheques including the printing of previously entered items.

3. Have any additional special so that the preset price can be changed during promotional period such as Happy hours in a bar.

4. Provide analysis of sales made by type of product and if required by a hour of trading.

5. Provide and analysis of sales by server per hour per shift period.

6.Analysis by method of payment for example cash, cheques, type of credit card etc.

7. Complete automatic tax calculations and cover and service charges.

8. Provide some limited stock control.

9. provide facilities for operator training to take place on the machine without disturbing any information already in the ECR.

10. restrict access to the ECR and the turtle draw by the key or code for each operator.

11. Have rotating turrent display of prices charged to individual customer transactions. This is of particular value in self-service and counter operations.

13. Eliminate the need for cashier by requiring each server to be responsible for taking payment from the customers and paying in the exact amount as recorded by the ECR at the end of each shift.

Electronic cash registers are not without their problem and it is important to consider the following try to select an ECR for purchase.

1. Is it suitable for the type and size of the operation it is to be used?

2. Cost -how does this compare with other models of similar capacity.

3. Is it an up to date model or is it about to be superseded?

4. Can this ECR be linked to similar ECRs as part of a network or directly to a microcomputer?

5. Maintenance. How foolproof is this machine? what level of maintenance is normally expected? Can simple maintenance be done by staff for example, changing of the printer ribbon etc.

7. What safeguards are standard or optional to the model when power failures occur?

Point of sale control systems-

At a basic level of point of sale control system is no more than a modern ECR with the additional feature of one or several printers at such locations at the kitchen or dispense bar. Some system replaces the ECR with "server terminal" which may be placed at several locations within a restaurant and is a modification of an ECR in that the cash features are eliminated making the terminal relatively small and inconspicuous.

The objectives for having printers are:

1. To provide an instant and separate clear and printed order to the kitchen or of what is required and by and for whom.

2. To speed up the process of giving the order to the kitchen or bar.

3. To aid, control in that items can only be ordered when they have been entered into the ECR or terminal by an identifiable member of the waiting staff and printed.

4. To reduce the time taken by the server in walking to the kitchen or bar to place an order, and as frequently happens, to check if an order is ready for collection.

5. To afford more time if required for customer contact.

Printers are at time replaced by VDU screens. Server terminals are part of a computer-based point of sale system. These special terminals are linked to other several terminals in the restaurant and bar within one system, and if required to, also interface with some other system, so that for example, the transfer of restaurant and bar charges may be made via the front office computer system. The advantage of computerized point of sale system is that it is capable of processing data as activities occurs which makes it possible to obtain up to the minute report for management who can be better informed and able to take immediate and accurate corrective action if necessary. This type of point of sale control system has been taken one step for the with the introduction of handheld terminals.

Remoanco's electronic service pad ( ESP) for example is palm size unit which uses radio frequencies to communicate from the guest's table direct to the kitchen and bar preparation areas. The use of such a terminal offers number of advantages: food and beverage orders are delivered faster and more efficiently to preparation sites; service in turn can attend more tables; with a two way communication service staff can be notified if an item is out of stock; all food and beverage items order are immediately charged to the guest's bill which is accurate and easy to read; finally operations can reassess their labour utilization and efficiency, certain members of the service staff, for example, can take the simple order while others can spend more time with customers to increase food and beverage sale.

The ESP is a completely noiseless terminal with orders being entered alphabetically numerically and by using preset codes. When not being used and the unit is closed its design resembles a conventional order pad compact and light in weight that can easily be carried around by service staff. It is currently being utilized in a variety of situations including restaurants and in launch areas.

Microcomputers-

before the invention of the microprocessor only a few large organizations were able to justify the high cost of computer system. In the hotel and catering industry this system was mainly applied to areas such as the front office, and reservation in particular, as well as for many aspects of the accounting functions. The very complex area of food and beverage management including purchasing, storing, stock control, standard recipes, menu planning, pricing, analysis etc. received scant attention from computer forms.

The information required by food and beverage management to be efficient it is demanding in term of computer programming storage and retrieval of data. The move from manual system to, system aided by mechanical cash registers, to system aided by the many type of ECR, has led to the evolution of totally computer edit control systems.

The reason for this evolution is simply that the computer equipment necessary for food and beverage control system is getting smaller, more powerful, cheaper, more reliable, less complex for and operator to use, and relevant software packages are available. The equipment required is of two kinds-

1. Hardware- the physical unit comprises the computer unit itself plus VDU printers and hard disk drivers.

2. Software- the computer programs designed and return to fulfill a specific purpose.

From the user's perspective software is seen as being in two major categories.

1. Packages- software that is bought in from a computer firm and is already pre-programmed to perform a specific function for example payroll stock control etc.

2. User developed program- software which is design by the food and beverage management staff or by company staff with or without the assistance of computer programming experti

in addition computer firms are marketing turnkey system which are pre-programmed software packages designed to serve a particular sector of the industry or to perform a particular function;they may also come with the necessary hardware. the basic of these marketing approaches is that it would be far too expensive to purchase computer hardware and then employ computer programming staff to write a specific set of programs for a unit or company.

The cost of computerized system would include:

1. The system hardware.

2. The system software.

3. The cost of additional and special programming.

4. The cost of training staff and payroll costs.

5. The cost of running a dual system while the new system is run- in an initial problems ironed out.

6. the cost of maintenance which should be by contract whenever possible.

7.the cost of supplies for example computer paper etc.

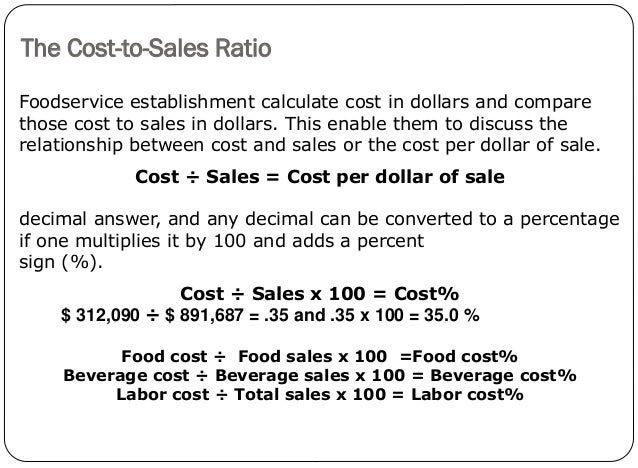

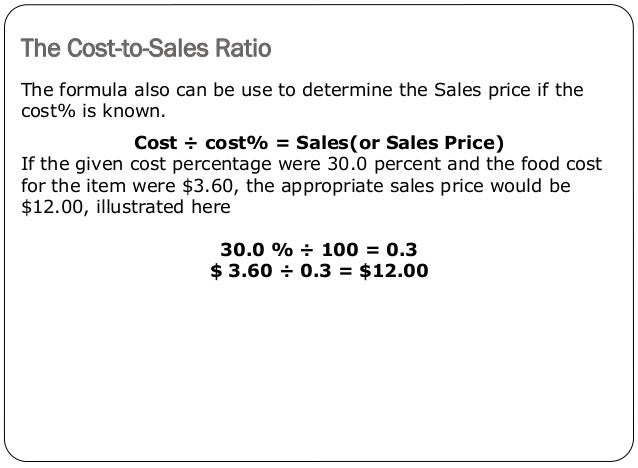

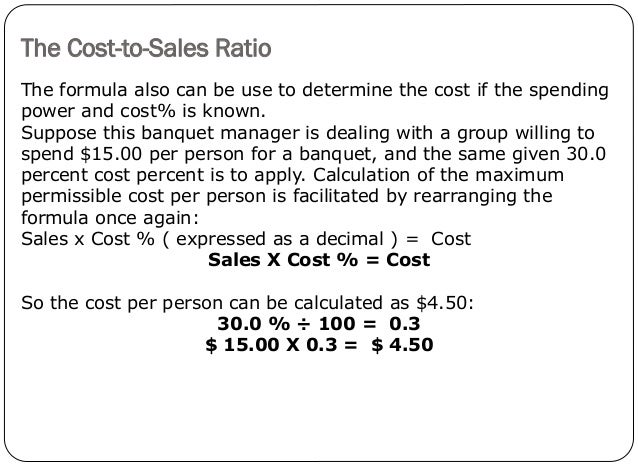

Operating yard sticks used in controlling-

Besides the general operating ratios that have been used earlier, for example food cost in relation to

food sales, beverage cost in relation to beverage sale etc.There are many more that are used and found

to be of value. The following is a brief explanation of those that are frequently used-

Total food and beverage sales-

The total food and beverage sales should be recorded, checked and measured against the budgeted sales figure for the particular period.

The analysis of these figures is usually done daily for large establishment and for those that are not operating manual control system. The analysis would show separately the food sales and the beverage outlet and permit period.

The importance of this yardsticks cannot be emphasized and other than to remind the readers that it is cash and cash only that can be banked and not percentage or any ratio or factor figures.

Departmental Profit-

As mentioned profit is calculated by deducting the departmental expenses from the departmental sales,

the expenses being the sum of cost of food and beverage sold, the cost of labour and the cost of overheads charged against the department, and the profit being usually expressed as a percentage of the departmental sales for example-

The departmental profit should be measured against the budget figure for that period.

Ratio of food and beverage sales to total sales-

It is worthwhile for food and beverages to be separated from each other and to express each of them as a percentage of total sales.This would be a measure of performance against the established standard busted percentage as well as indicating journal train in the business.

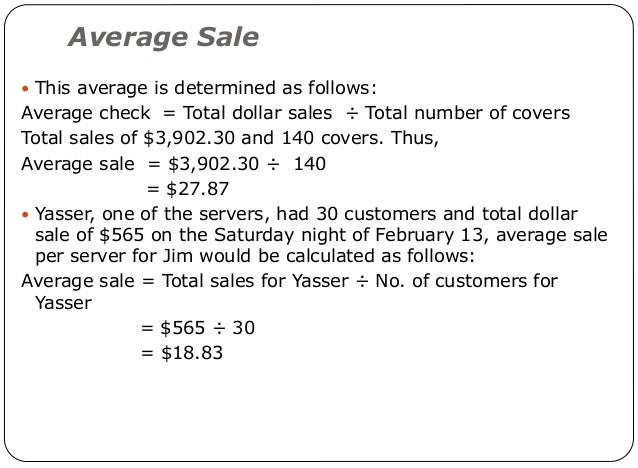

Average Spending Power-

This measures the relationship between food sales and beverages to the number of customer service if food sales are Rs.350 and the number of customer service is 70 the average spent by each customer is Rs5(350/70=5)the average spending power for beverages usually related to the number of item recorded on the bill roll rather than to the number of customers and the total average sales. Thus if rs. 600 is the recorded beverage sales and an analysis of the till role show that 400 drinks had been sold the average spend per check would be Rs 1.50. What is different here is that a customer mein order several drinks during an evening and therefore the average amount spent on a drink is more important than the ASP per customer to calculate the ASP for bottled wine sale in a restaurant or at the banquet though could be a useful exercise.

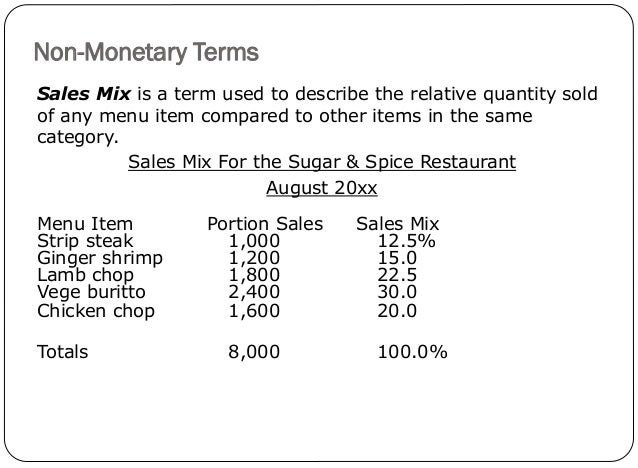

Sales Mix-

this measures the relationship between the various component of total sale of a unit for example

Sales mix. %

Coffee shop sales

Food. 20

Beverage. 5

Restaurant sales

Food. 25

Beverages. 15

Banqueting sales

Food. 20

Beverage. 10

Cocktail bar sales

Beverage. 5

Total = 100

In addition of sales mix may be calculated for the food and beverage menus for each outlet under group heading suggest appetizer, main course items, sweet course, coffee etc and spirits cocktails beers and largers etc.

Payroll costs-Payroll cost are usually expressed as a percentage of sales and are normally higher the higher the level of service offered. It is vital that they are tightly controlled as they contribute high percentage of total cost of running and operation.

Payroll cost can be controlled by establishing headcount of employees’ department for establishing the total number of employees are allowed per department in relation to a known average volume of business. In addition all overtime must be strictly controlled and should only be permitted when absolutely necessary.

Index of productivity-

This is calculated by the formula = Sales/ payroll (including any staff benefit cost)

The index of productivity can be calculated separately for food sales, beverages sales or for total food and beverage sales.

The use of the term payroll

cost in the formula includes not only the appropriate payroll cost but also any other employee benefits such as employees pension contribution medical insurance etc.

The index of productivity would vary depending on the type of operation, for example a fast food restaurant with takeaway service would have a high index of productivity, as the payroll cost would be lower than a luxury restaurant employing highly skilled and expensive staff with high ratio of staff to customers which may have a relatively low index of productivity.

s petrol cost can be controlled and should be related to the forecasted volume of business standard index of activity can be established to measure how accurately the two elements are related.

Stock Turnover-

It is calculated by the formula = Rate of stock turnover= cost of food or beverage consumed/average stock value.

The rate of stock turnover gives the number of times that the average level of stock has turn over in each period.

Too high turnover would indicate very low level of stock being held and many small value purchase being made. This is costly and time consuming for whoever does the purchasing as well as costly for the purchase as no price advantage can be taken off the standard quantity offer made by the suppliers. Too low turnover would indicate unnecessary capital tied up in an operation and therefore addition a large control and security problem.

Sales per seat available-

This shows the sales value that can be earned by a seat in a restaurant like coffee shop.

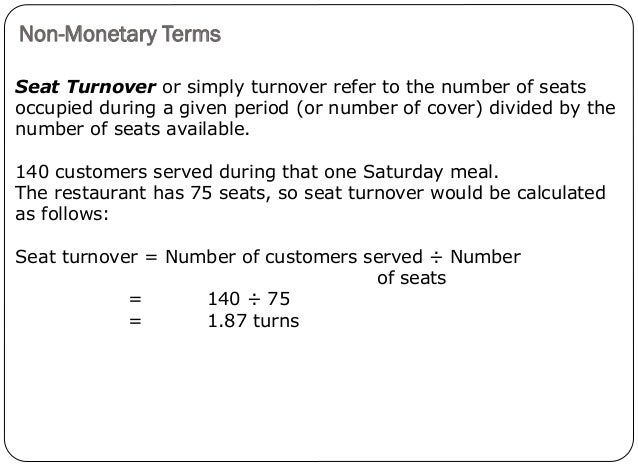

Rate of seat turnover-

This shows the number of times that a seat in a restaurant like coffee shop is used by customers during a specific period does if in a 120 seater coffee shop 400 customers was served in 3 hour lunch period the rate of seat turnover would be 400 / 120 that is 3.33. As the coffee shop staff can only sell food to customer while they are seated at table the importance of the rate of seat turnover is highlighted.

Sales per server-

Hit server will have a known number of covers for which he is responsible. This would vary depending on the style of food and beverage service offered. SS people for the restaurant or coffee shop there taking should be of a predetermined target level to contribute to a satisfactory level of turnover and profit.

Sales per square foot/meter-

This is a self explanatory in that the space of all selling outlet need to be used to its base advantage Aaj so as to achieve desired turnover and profit. This can be calculated on a square feet or meter basis.as the square footage per customer varies with the type of food and beverage service of food so must the cost to the customer so that the establishment is earning the desired turnover and profit per square foot of selling space.

Thanks sir ..

ReplyDeleteMayank 019112216

DeleteNimit Makhija -09411002216

ReplyDeleteRithika Dahima: 01811002216

ReplyDeleteAkhil chopra 03211002216

ReplyDeleteSiddharth Mahajan 07211002216

ReplyDeleteSanjan Kapur (07411002216)

ReplyDeleteThank you sir , vakul-04711002216

ReplyDeleteAbhishek Nagpal-061

ReplyDeleteHarshdeep Singh - 04311002216

ReplyDeleteAayush yadav-055

ReplyDeleteDhruv grover- 09611002216

ReplyDeleteNitish george 064

ReplyDeleteSumit samal 044

ReplyDeleteThank you for sharing notes..

ReplyDeletePratha Mathur - 07311002216

085 daljeet singh

ReplyDeleteAvneet Singh 099

ReplyDeleteVishal Madan (049)

ReplyDeleteKirat singh 091

ReplyDeleteSanjan Kapur - 07411002216

ReplyDeleteKirti 054

ReplyDeleteRaghav rathi -10011002216

ReplyDeleteVinit Kumar 00811002216

ReplyDelete05711002216 - harsh saxena

ReplyDeleteHarshit Mishra

ReplyDelete11311002216

Shruti yadav-10811002216

ReplyDeleteThank you sir Mohit DHAWAN:+ 12211002216

ReplyDeleteVilakshan Mehta

ReplyDelete12911002216

Thank you,sir

This comment has been removed by the author.

ReplyDelete054 Kirti

ReplyDeletePratham 06811002216

ReplyDelete12611002216

ReplyDeleteTanveer Singh Randhawa

ReplyDelete01011002216

Balvinder Singh

ReplyDelete06611002216

054 Kirti

ReplyDeleteHarshpreet Singh

ReplyDelete09011002216

Kamal Vashisht 11611002216

ReplyDeleteKirti 054

ReplyDeleteSoumitra Chaturvedi 02911002216

ReplyDeleteSiddharth kukreja

ReplyDelete08711002216

Taha Saleem - 037

ReplyDelete114 11002216

ReplyDeleteArchit

Hina Maken

ReplyDelete(082)

Gaurika Chaurasia (053)

ReplyDeleteShashank : 10511002216

ReplyDeleteROMIL ADVIN HARRISON ROLL 036 A BATCH

ReplyDeleteAbhishek Vats-028

ReplyDeleteSagrika- 059

ReplyDeleteAbhinav Sharma

ReplyDelete107

107

ReplyDeleteSaheb 088

ReplyDeleteTarandeep Singh - 07711002216

ReplyDelete04111002216 Mahin

ReplyDelete03911002216

ReplyDeleteSiddharth verma

04911002218

ReplyDeleteRahul Thapa

Sumit Lathwal

ReplyDelete12711002218

Pankaj dangwal-12611002216

ReplyDeleteAbhishek Maheshwari :- 06711002216

ReplyDeleteIshmeet singh

ReplyDelete12511002218

Mohd aamir qureshi

ReplyDelete12411002216

Pawan Kumar

ReplyDelete05711002218

Bhavandeep singh07011002216

ReplyDelete